Medium Term Forecast 2026–2029, Spring Edition

A. International context and risks

Uncertainties and downside risks to the economic outlook intensified at the beginning of 2026 at both global and regional level, against the backdrop of the protracted conflict in Ukraine and the escalation of a new conflict in the Middle East. The latter generated an energy shock affecting all oil, natural gas, and fuel‑importing countries in the region, disrupting not only the supply of energy products but also global supply chains for chemical fertilizers and other goods transiting the area.

The impact was felt most acutely by Asian countries dependent on oil and natural gas from the region, with energy product prices reacting rapidly and reaching historical highs in the second quarter of the current year. Subsequently, the price surge propagated to other regions, with international institutions expecting a deceleration in economic growth across most economies. At the same time, disruptions in fertilizer supply along regional routes could affect agricultural production in importing countries, adding further pressure on agricultural and food prices.

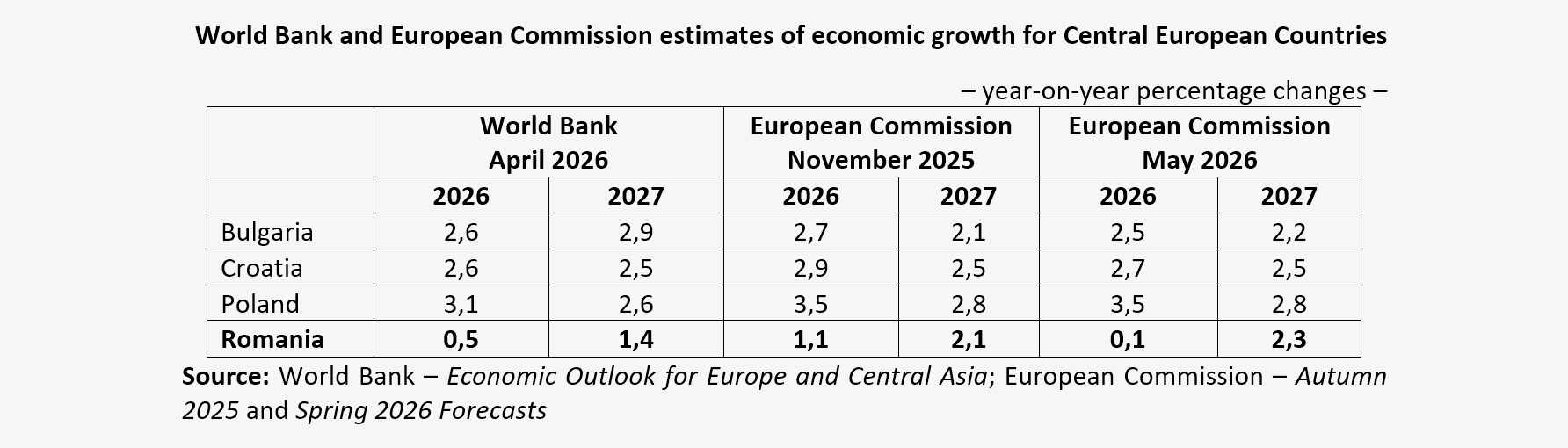

In this context, the World Bank’s April forecast for Central Europe marked downward revisions compared with estimates from the beginning of the year, by 0.3 percentage points for 2026–2027. The adjustments applied to all countries in the region (Romania, Croatia, Bulgaria, and Poland). In January, the World Bank estimated that the global economy would grow by 2.6% in 2026 and 2.7% in 2027, with expectations supported by the significant resilience shown in 2025 in the face of the new U.S. trade policy and geopolitical tensions. For Central European countries, growth is expected to reach 2.7% in 2026, with a similar level projected for the following year.

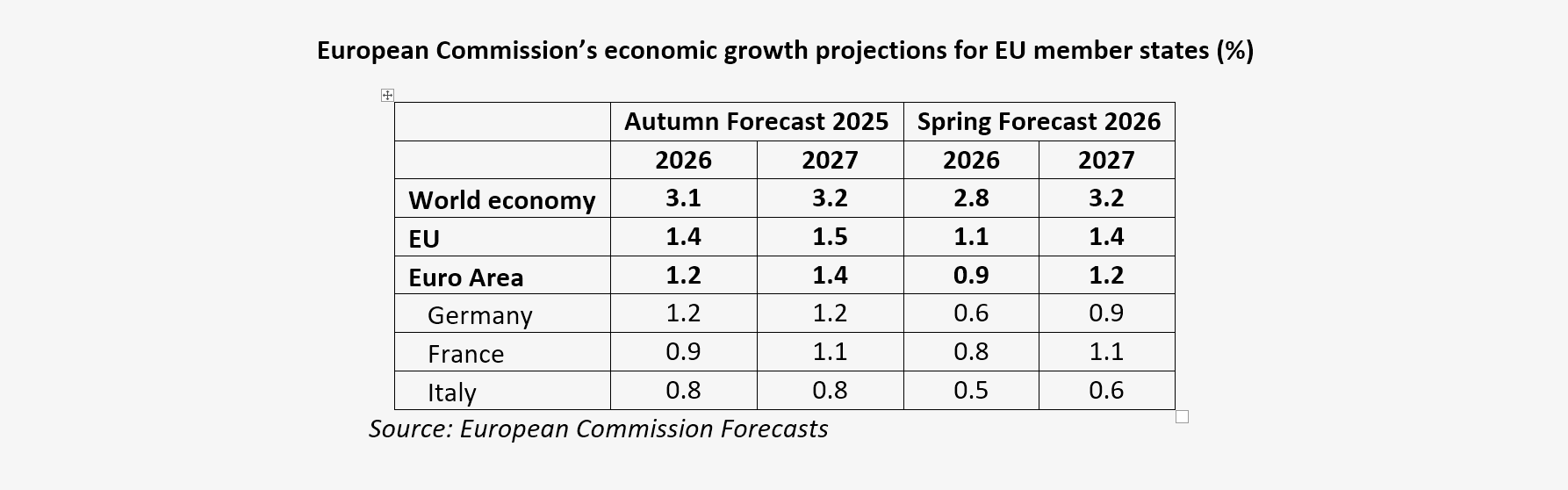

Recently, the European Commission also revised down its forecast for the economies of the European Union by 0.3 percentage points, to 1.1% for 2026 and 1.4% for next year, and for the euro area to 0.9% and 1.2%, below the levels projected in autumn. The revisions were applied to most Member States.

For Romania, the World Bank projected 0.5% economic growth for this year, which is 0.8 percentage points below the level estimated in January, followed by a recovery to 1.4% in 2027. The World Bank considers that public investment, including from EU sources, will partially offset the decline in consumption that occurred amid the government’s fiscal consolidation efforts.

The European Commission estimates that Romania’s economy will advance only marginally in 2026 compared with the previous year, with activity close to stagnation (+0.1%), before accelerating to 2.3% in 2027. Fiscal consolidation efforts and elevated inflation, driven by rising energy prices, will reduce domestic demand. EU‑funded investment and net exports will make a positive contribution, mitigating the losses stemming from weaker consumption.

The recovery in 2027 will be supported by lower inflation and more favourable financing conditions. Unemployment is expected to increase moderately in 2026, before declining to 5.9% in 2027. The current account deficit is projected to improve to 6.4% of GDP over the forecast horizon.